We all make mistakes.

Sometimes these errors are minor, but other times they are grave. You need to learn how to avoid these mistakes.

Launching your own business is no easy task. As someone who has helped multiple startups to get off the ground, I know this process firsthand.

Things don’t always go as planned. Research shows that 90% of startup companies fail.

Sure, everything looked good on paper. You found the perfect name for your startup, but you hit some speed bumps along the way that you may not have been prepared for.

If your most recent business venture didn’t work out, it’s nothing to be ashamed of.

I get it. You poured your heart and soul into this project. The failure seems tough to overcome, especially if it cost you some money.

But your story doesn’t need to end here. You want to be an entrepreneur. That’s why you attempted to launch a business in the first place.

Don’t just accept defeat and try to get a standard nine-to-five job like everyone else out there. I know plenty of people who couldn’t get their startup off the ground.

You have two paths from here. You can either quit or move forward. Don’t fall into the group of entrepreneurs who quit.

I’ll show you how you can take that failed launch and turn it into an advantage that will move you forward. Here’s what you need to do.

Take a break

Launching a startup doesn’t happen in a week.

It starts with careful planning and research and then implementation of your ideas. You went through all the legal requirements of incorporating your business.

You spent time and money to develop products or software. Maybe you even built a mobile app.

Being an entrepreneur isn’t for everyone. That’s why they make up the smallest population of the workforce across the globe.

Everyone’s situation is different. Your startup could have failed after a couple of months or even a couple of years.

But regardless of when you failed, I’m sure you put in tons of hard work. You had some long hours and sleepless nights.

Working this hard over an extended period of time can burn you out.

It’s possible the effect of this failed launch even impacted your personal life.

You don’t want to let this event negatively affect the relationships with your family and friends. These relationships are much more important than your business.

Use this time as an opportunity to correct any wrongdoings that may have occurred while you were working on the startup.

Step away and just relax.

I realize this can be tough, especially if you don’t have a steady source of income at this moment. But you need to find a way to recharge your batteries.

As crazy as it sounds, taking a vacation might be just what you need. Put your startup out of your mind. Focus on your physical and mental health before you do anything else.

Once you have a chance to clear your mind, it will be much easier for you to jump back on the horse for a fresh start.

Figure out what went wrong

Now that you’ve had a chance to take your mind off things for awhile, it will be easier for you to assess the situation—you’ll have a more objective perspective.

You need to be able to look at yourself honestly in the mirror. It’s time to determine why your startup failed.

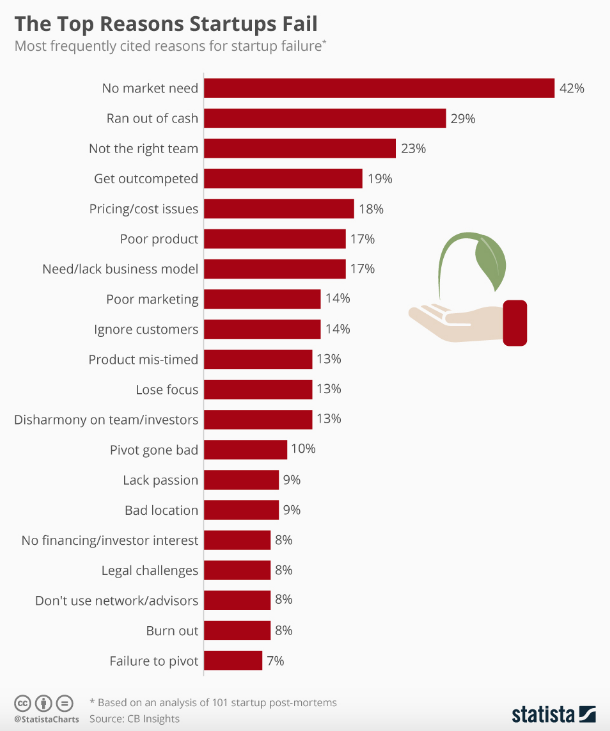

While it may be easy or convenient to blame someone else, you need to take responsibility for your actions. Here are the top reasons why startups fail:

If you look through this list, you’ll see many of these scenarios could have been avoided.

As the founder of your startup, you are responsible for making sure everything goes according to plan.

Let’s review the top three reasons for startup failure.

1. No market need

The number one reason why startups fail is because there wasn’t a market need. This should have been discovered during the early stages of the business. It’s your responsibility to conduct the proper market research. One of the first steps of launching a new business is to identify the target market of your startup.

If you skipped this step or took some shortcuts through the process, it could be the reason why you failed. Learning there was no market need for your startup could have saved you a ton of time, money, and effort if you figured this out in the early weeks or months.

2. Running out of cash

Running out of money could happen for a few reasons. Perhaps you either didn’t raise enough money or didn’t budget accordingly.

Again, both of those scenarios would fall on your shoulders.

Don’t get me wrong here, I’m not saying this so you can beat yourself up about it.

I just want you to figure out exactly what the problem was. Being in denial won’t help you move forward and turn your failure into a success story.

3. Not the right team

Surround yourself with people who can help you succeed. As you can see from the graph above, 23% of startups failed because the team wasn’t right.

Rather than blaming your team members for the demise of the company, make sure you find the proper people moving forward.

After all, who hired those team members? Don’t bring someone on board if they don’t bring anything to the table.

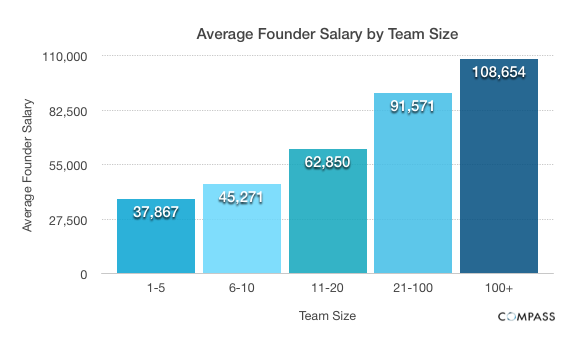

Research shows that founders with larger teams are able to pay themselves higher salaries.

But doesn’t mean you should be hiring a ton of people right away.

Make sure you work with people who are compatible with your management style, hard working, and skilled in areas where you are weak.

For example, let’s say you are an excellent marketer. Working with a partner who is also a great marketer may not be what you need if neither of you knows how to develop products or handle finances.

Don’t lose confidence

Failure can be an extremely humbling experience.

But you need to be able to find the balance between being humble and remaining confident.

Entrepreneurs typically have that “eye of the tiger” character trait that gives them an edge in life. Don’t lose that feeling and mentality just because of a mishap.

Sure, you may not approach your next venture with that feeling of invincibility you had when you started your last one, but you should always remain confident in yourself.

Your failed startup is just one minor event on the long timeline of your life. Don’t let it define you.

Instead, use it as motivation to bounce back and be better than ever.

Trust me, you weren’t the first person, and you certainly won’t be the last, who failed at something. People have been in situations far worse than yours.

Look at the positives in your life. You’ve got family, friends, and your health. Be thankful for what you have.

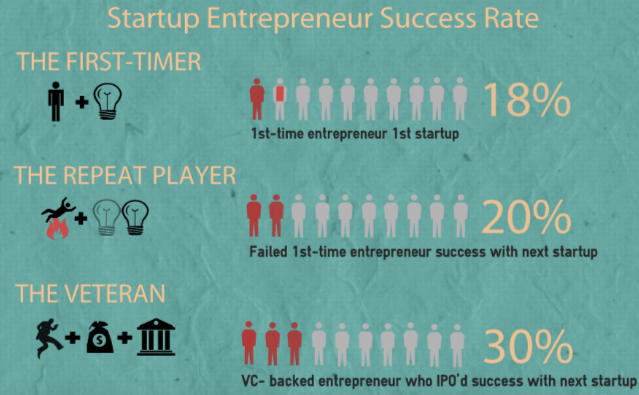

I have some encouraging news. The next time you launch a startup, you’ll have a greater chance of succeeding:

This makes sense.

That’s because you’ve been through this process before. It won’t be as overwhelming the next time because you’ll know what to expect.

Learn from your mistakes

Now that you’ve taken the time to recognize what went wrong, learn from those mistakes.

During what stage did your startup fail? Was it before or after the launch?

Did you have problems with production? Was there an issue with your product?

The key is to make sure you don’t make the same mistakes twice. You can’t just blindly approach your next startup without keeping your previous mistakes in the back of your mind.

Don’t take any shortcuts. Make sure there is a market for your brand. Secure the proper funding to reduce the chances of running out of money.

Bring in a partner or two if you need help. But it’s important to make sure everyone involved has a clearly defined role.

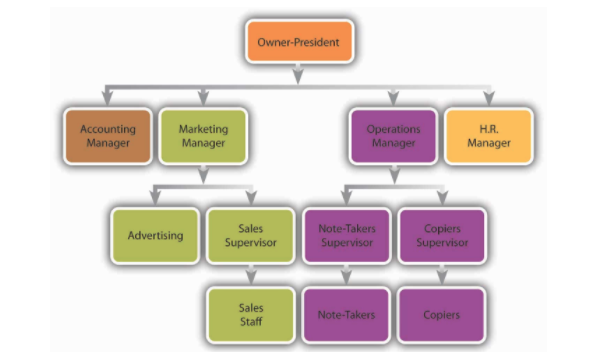

Here’s a look at the typical organizational structure of a business:

Obviously, these titles will vary based on your type of business. But you can still use this as a reference so everyone clearly understands the management hierarchy.

Don’t be so hesitant to raise money from outside investors.

You’ll have less equity in the company, but you won’t be crippled financially if things end up going wrong again.

Plus, the fact that others will have a stake in the business will make them care more too. They will also put in the effort to make sure the company is successful because they have money on the line as well.

Focus on your concept

Take the time to put some effort into your concept whether it’s:

- a product

- a service or

- software

I’m assuming your idea falls into one of these three categories or potentially a combination of them.

Ask yourself these questions: Do I need to start from scratch? Or can I make a variation of my failed attempt?

Sometimes, you may not need a completely new idea for a business. On the other hand, it may be in your best interest to start over with a new concept.

Everyone’s situation is unique.

It’s possible your product or concept wasn’t the issue that led to the failed launch. There may have been problems with budgeting, marketing, or some other factor that hindered your success.

If that’s the case, you could just launch another startup with the same concept under a different name.

Develop a detailed business plan

After you’ve taken the time to analyze your failure, it’s time to get back on the horse.

Whether you’re going to launch with the same concept or a new one, you have to start with a business plan.

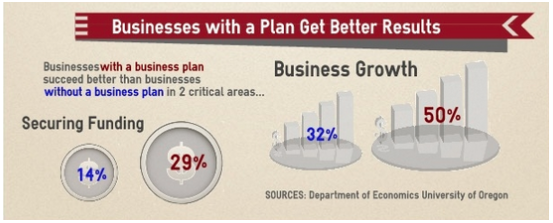

Learn how to write a business plan for your startup. Business plans will keep you accountable for your actions. If you put something on paper, you’ll make the effort to follow through with it.

Plus, writing a business plan increases your chances of securing funds and growing your business.

As a result, your chances of success will be much higher.

The first step of writing a business plan is clearly defining your target market. This will tell you exactly whom your brand is for.

Research your competitors. Is your product already available on the market? With whom are you competing?

This will help you come up with a strategy separating you from the crowd.

Set a realistic budget. Recall our discussion about investors. Make sure you raise enough money so that you don’t have to worry about running out of cash.

Include a financial section of your business plan. When will you break even? Display your cash flow projections and expenses.

Account for everything to make sure you can survive until you have a steady income.

Your business plan should include a plan to market your startup company.

Conclusion

If your new idea for your business feels like it has legs, go for it.

Be confident in yourself and this new idea. Go through the steps carefully without taking any shortcuts.

Just don’t rush into things. It’s important for you to take a break in between these launch attempts. Take the time to analyze what went wrong so you can learn from your mistakes and avoid repeating them.

Entrepreneurship isn’t for everyone.

Don’t feel obligated to start a new business right away if you’re not ready. You may decide to try something else in the meantime.

But as we discussed earlier, you’ll have a greater chance of succeeding the next time around, so don’t be discouraged by what happened in the past.

Turn your idea into a reality.

How were you able to identify what went wrong with your first startup launch?

from Quick Sprout https://ift.tt/2LaPzct

No comments:

Post a Comment