If you want to accept credit card payments from your customers, you need to find a payment processing service. This holds true for both ecommerce and in-person retail sales.

However, all credit card processors are not the same. So it’s tough to name one as the definitive best option.

Finding the right credit card processing service for your business is crucial, since the fees, performance level, and customer experience will vary based on your choice.

An ecommerce giant and small local coffee shop shouldn’t be using the same processing company.

Whether you’re looking to switch processors or you’re accepting credit card payments for the first name, this guide will help steer you in the right direction. My methodology will make it much easier for you to find the perfect credit card processing service for your business.

The 8 Best Credit Card Processing Services

The credit card processing industry has become extremely competitive over the years. With ecommerce on the rise, companies have adapted accordingly. New players are emerging in this space as well.

But with so many options to choose from, there are really only eight different payment processors that I would recommend.

You’ll likely be familiar with at least a couple of these names, but others are lesser-known.

For each processor, I’ll breakdown the pricing, benefits, drawbacks, and explain which types of businesses should consider the processing service.

Stripe

If you’re accepting payments online, Stripe should be one of your top choices. In fact, Stripe ranked first on my list of the best payment methods for your ecommerce site.

Stripe is built for developers, so you might be a little overwhelmed when you first land on their website. However, you’ll quickly realize that this payment processor is easy to use, regardless of your technical experience.

For those of you who want to take advantage of the developer features, you’ll be impressed with the Stripe API and UI toolkit.

Another top benefit of Stripe is its built-in fraud protection system. This will help you manage and avoid ecommerce chargebacks.

It’s easy to integrate Stripe with your ecommerce store, regardless of the platform that you’re using. Stripe accepts a wide range of payment options, including digital wallets like Apple Pay, Microsoft Pay, Google Pay, and Visa Checkout.

Stripe helps simplify your checkout process. According to a recent IDC report, businesses using this payment processing service were able to increase their revenue by 6.7%.

The report also found that Stripe resulted in 59% higher productivity, 81% fewer unplanned outages, and 24% lower operating costs.

Speaking of costs, Stripe is an affordable payment processor, even if you’re just starting out. The fixed pricing model is very straightforward:

- Online transactions — 2.9% + $0.30

- International cards — Additional 1% per transaction

- Currency conversion — Additional 1% per transactions

- ACH debits — 0.8% with a $5 max per transaction

- In-person payments — $2.7% + $0.05

If you use Stripe to set up recurring charges for subscription customers, your first $1 million is free. After that, you’ll pay $0.5% on all recurring charges.

I like Stripe because you pay the same flat rate for all credit cards, including digital wallets and premium cards like American Express.

For those of you with unique business models and large payouts, you may qualify for a customized pricing solution. Contact the Stripe sales team about volume discounts, interchange pricing, and multi-product discounts.

Overall, Stripe is an ideal solution for any ecommerce business. It is highly technical, which can be a drawback for companies that don’t have a developer on staff.

Helcim

Helcim is an all-in-one payment processing service for retail locations and online stores. It’s a top choice for small business owners.

Transparency is the reason why Helcim ranks so high on our list. Their interchange pricing structure shows you exactly how much you’ll pay above the interchange rate set by the credit card companies.

Helcim has arguably the best rate guarantee in the industry. They will never increase your rates for the lifetime of your account. While the fees for certain cards might go up, the Helcim margins will always remain the same.

When you sign up for Helcim, you’ll choose between two base plans:

- Retail — $15 per month

- Online — $35 per month

While Helcim does have the online feature, I’d personally just consider them for in-person payments.

Your rates will vary by industry, monthly processing volume, and average transaction amount.

The industry options are:

- Retail

- Restaurant

- Online

- Charities

- Real estate and property management

- Online international

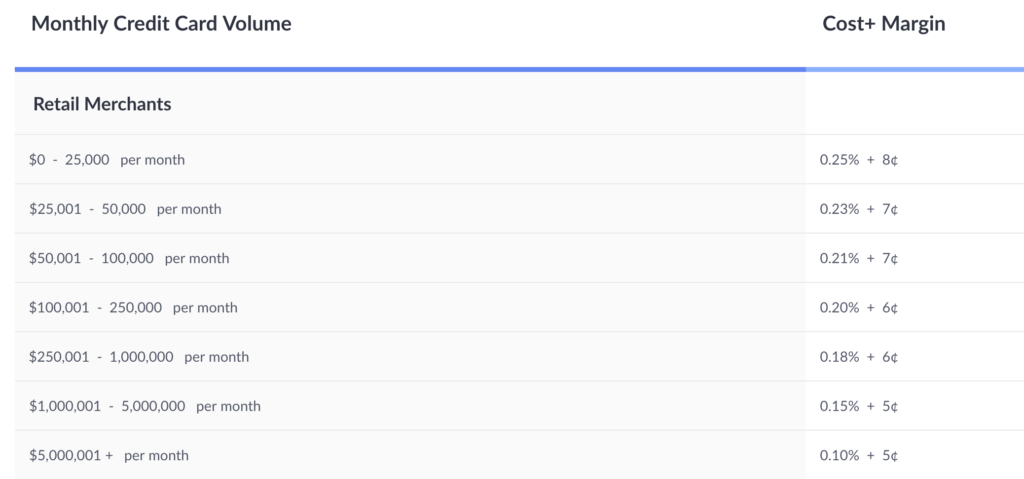

Here’s a detailed look at the pricing rates for retail merchants based on monthly volume.

If you compare these rates to other processing services out there, you’ll see that Helcim interchange pricing costs are below average. So it’s an excellent way for small businesses to save some money on credit card processing, even if they are in the lower pricing tiers.

Helcim contracts are month-to-month, and they don’t charge any cancellation fees.

You can integrate Helcim with QuickBooks to improve your small business accounting process as well.

Helcim offers a POS system, with an app that’s free with your plan. However, the app does not integrate with the credit card terminals as of now, which isn’t ideal. Terminals purchased through Helcim range from $229 to $649 per unit.

While Helcim prices are competitive and generally low, it’s not the best choice for those of you who are only processing less than $3,000 per month. You can probably find a more cost-effective alternative elsewhere.

Square

More than 2 million businesses use Square to process payments. Square offers POS systems with built-in payment processing. This company ranked first on my list of the best POS systems, so the fact that they double as a payment processor is an added bonus.

Any business accepting in-person payments needs to take a closer look at Square.

Square also processes payments online, on the go, through recurring invoices, and manually for orders taken over the phone. But with that said, the in-person POS processing is where Square really shines.

Another standout of Square is the ability to get paid fast.

While most processing companies usually take a couple of days for funds withdrawals, Square gets money in your bank account in the next business day. They also offer instant transfers for a fee.

Square’s pricing is straightforward and transparent. You’ll pay the same rate for every card, including Discover and American Express.

They don’t charge any startup fees, monthly fees, cancelation fees, authorization fees, statement fees, terminal fees, or other common industry-standard markups.

Square pricing varies slightly by industry and POS hardware, but here are the most common rates offered:

- Square Point of Sale — 2.6% + $0.10 per transaction

- Square For Retail — 2.5% + $0.10 per transaction

- Ecommerce transactions — 2.9% + $0.30 per transaction

- Card not present transactions — 3.5% + $0.15 per transaction

- Card on file transactions — 3.5% + $0.15 per transaction

Square provides you with everything you need for success when processing payments. They have active fraud prevention, account takeover protection, dispute management, other security measures like PCI compliance and end-to-end encryption.

Signing up and getting started with Square is simple.

The only major drawback of Square is that its customer service is not available 24/7. Most processing companies can be reached on weekends, nights, or other odd hours.

If I were running a physical retail store and wanted a POS system and payment processor from the same company, I’d choose Square.

PayPal

PayPal has been a giant in the world of processing transactions for more than a decade. It’s a name that we’re all familiar with, and there’s a good chance that you’ve used PayPal in some form or another in your personal life.

While PayPal has always been known for its P2P payments, it’s also a great choice for businesses to use as a payment processing service.

You can use PayPal to accept payments both online or in-person. It’s the best option for low-volume businesses to get paid online.

I recently wrote an article comparing PayPal vs. Stripe for ecommerce. While Stripe definitely has its fair share of advantages, the PayPal technology is much simpler. It’s also extremely easy to set up. You won’t need to worry about all of the developer features like you do with Stripe.

Let’s take a closer look at PayPal’s processing fees:

- Online payments and invoicing — 2.9% + $0.30 per transaction

- Mobile and in-store payments — 2.7% per transaction

- Manual entry transactions — 3.5% + $0.15 per transaction

As you can see, the pricing is nearly identical to Stripe.

One of the best parts about using PayPal as your online payment processor is that you’ll be able to accept PayPal, Venmo, and PayPal credits in addition to all major credit and debit cards.

This is a massive advantage over other payment processors, where you would need to integrate PayPal separately.

While I personally like PayPal’s online features, the flat rate of 2.7% per transaction for mobile and in-store payments is appealing for low-volume merchants as well.

The biggest downside of using PayPal is that customers will be taken to the PayPal website to finish processing all online transactions. You can eliminate this step and integrate PayPal directly into your site, but there is an added fee for that.

Speaking of added fees, PayPal has a long list of add-ons and other incidentals that they charge for. They are transparent about these prices, but make sure you review all of them in your contract so you fully understand the terms.

Overall, you know you’re getting a trusted and reputable brand if you use PayPal to process credit card transactions for your business.

Flagship Merchant Services

Flagship Merchant Services is a bit different compared to other credit card processors that we’ve reviewed so far. If you land on their website, you’ll quickly see that there aren’t prices listed anywhere.

In fact, their website is just one page. There’s nowhere to really navigate and learn much more about their services.

The benefit of Flagship Merchant Services for credit card processing is that everything is totally customizable. They offer flexible terms and month-to-month pricing for all businesses.

Types of pricing plans are customizable as well. Flagship Merchant Services has tiered pricing and interchange plus options, whereas other payment processors typically just offer one or the other.

More than 25,000 small business owners trust Flagship Merchant Services to process their credit card payments.

While this payment processor might be a bit smaller or lesser-known than some of the other options on our list, working with a smaller company has its benefits.

Flagship Merchant Services offers exceptional 24/7 customer service. You’ll get a free EMV terminal or Clover Mini POS system when you sign up. If they can’t lower your processing rates, they’ll send you a $50 AMEX gift card.

The downside of this payment processor is the setup and getting started. No prices or contract details are available online. So you’ll need to speak to a sales rep to request a quote, which isn’t convenient for everyone.

Payment Depot

Payment Depot processes more than $4 billion in credit card sales with over 3 million transactions per month. Their system is simple; they charge a membership fee to give you access to wholesale processing rates.

Think of Payment Depot as the Costco for credit card processing. The prices are lower than the competition, but you need to be a member.

For this reason, Payment Depot is the best option for high-volume merchants.

Payment Depot does not take a percentage of each transaction. They simply charge a fixed amount per transaction based on your membership tier on top of the interchange fee.

Here’s an overview of the plans, features, and pricing:

Basic — $49 per month + interchange

- $25,000 monthly processing limit

- $0.15 per transaction

- Reprogram your existing equipment for free

- Free gateway

Most Popular — $79 per month + interchange

- $75,000 monthly processing limit

- $0.10 per transaction

- Free standard terminal

- Data breach protection

- Premier 24 hour support

Best Value — $99 per month + interchange

- $200,000 monthly processing limit

- $0.07 per transaction

- Free standard terminal

- Free pin pad

Premier — $199 per month + interchange

- Unlimited processing

- $0.05 per transaction

- Free standard terminal

- Free pin pad

- Free terminal upgrade every two years

All plans come with a 90-day free trial.

Payment Depot is used by big brands like Dominos, Boost Mobile, Subway, Arco, and Sprint. I wouldn’t consider this payment processor unless you’re over the $25,000 monthly limit.

As you can see from the rates, you can save lots of money on processing fees with a Payment Depot membership.

Overall, this is an impressive payment processing service. The only downside is that it’s not realistic for most smaller businesses to consider.

CDGcommerce

CDGcommerce offers custom credit card processing services for different industries. Some popular categories include:

- Retail

- Restaurant

- Service

- B2B

- Ecommerce

- Nonprofit

Clearly, all of these different business types will have varying needs. But overall, CDGcommerce is the best choice for nonprofit organizations.

That’s because CDGcommerce doesn’t charge any monthly fees or require monthly minimums for nonprofits. You can get an integrated mobile card reader, set up recurring billing, and benefit from special nonprofit rates.

The rates will vary based on volume and specific needs, but nonprofit processing typically starts 0.20% + $0.10 per transaction, plus interchange costs.

If you fall into one of the other categories, CDGcommerce has flexible pricing options based on your monthly volume.

One Rate Pricing: $1,000 – $10,000 monthly volume

- Flat rate and fixed monthly fee

- Customer tracking

- Loyalty promotions

- Invoicing, virtual terminal, ecommerce solutions

- Fully integrated credit card terminal

- Nonprofit campaign and donation management

Interchange Plus Pricing: $10,000 – $200,000 monthly volume

- Full transparency

- Pass-through pricing

- $100,000 data breach protection plan

- PCI security tools and solutions

Wholesale Membership: $200,000+ monthly volume

- Discounted pricing based on annual membership

- All benefits of the other plans

Again, the specific rates will vary for each business based on a number of factors. You need to contact the CDGcommerce sales team to request a quote.

I chatted with an online sales rep just to see how long this would take, and I got a quick answer in just a couple of minutes. This wasn’t an official quote, but it’s nice knowing that they are quick to respond. That’s where I got the starting rates for nonprofits, which isn’t listed anywhere on the website.

Payline

Payline is another lesser-known payment processing service. But they have a wide range of solutions for mobile payments, ecommerce payments, and in-person payments.

They can meet the needs of small business owners, enterprises, and everyone in between.

However, Payline is the best option for a very specific type of business—high-risk merchants.

For one reason or another, certain merchants are considered a high risk to credit card processing companies. It could have to do with the history of your company, or maybe it has to do with the types of products that you’re selling (CBD, firearms, vaping, etc).

It’s tough for these merchants to find a credit card processing service that will work with them, and even harder to find one that will offer favorable rate terms.

So if you fall into the high-risk merchant category, Payline will be your best option.

Payline will even work with businesses in online gaming, casinos, multi-level marketing, and adult industries.

Rates and plans are customized for each merchant. But if you’re struggling to find a payment processor that will accept your business, I’d schedule a call or apply online with Payline.

How to Find the Best Credit Card Processing Services

There are certain features that you need to keep an eye on when you’re evaluating a credit card processing service. This is the methodology that we used here at Quick Sprout to filter results and come up with the list above.

Pricing Type

There are two main pricing structures for credit card processing.

- Fixed

- Interchange

With fixed pricing, it’s the same rate for each transaction, regardless of the credit card that the customer uses. Stripe, Square, and PayPal are examples of processors with fixed prices.

For interchange pricing, you pay the amount charged by the credit card company, plus the markup fees of the processor. Helcim has interchange pricing.

Flagship Merchant Services offers both fixed-rate plans as well as interchange pricing, since they provide custom solutions for different businesses. Some credit card processors, like Payment Depot, will charge you a monthly rate to access wholesale prices.

It’s crucial to figure out which pricing structure works best for your business because the structure will ultimately affect how much you pay.

Monthly Volume

In most cases, high-volume merchants can get lower processing rates per transaction. You can request a custom quote from nearly every credit card processor, even if they have fixed rates advertised on their website.

With that said, there are certain services that are best for high-volume merchants, and others that are better for low-volume merchants.

I’d recommend PayPal for low-volume processing and Payment Depot for high-volume credit card transactions.

Industry

The type of business you have will affect your credit card processing terms. Rates vary if you’re processing cards online, in-person, or over the phone for “card not present” transactions.

Stripe is the best provider for online transactions, while Square is better for brick-and-mortar retail locations.

Other payment processing services specialize in nonprofit organizations or high-risk merchant industries. So if you fall into one of those categories, you’ll need to find a processor that can meet those needs.

Funds Withdrawals

How soon can you get your money?

In most cases, funds are available in your bank account after two business days. Sometimes this period can be a bit longer when you’re just starting out.

Other credit card processors offer next-day delivery for funds. Some providers will let you do an instant funds withdrawal for an added fee. So if you need your money immediately, this is definitely something that you need to keep in mind.

Extra Costs

In addition to the transactional fees or monthly plan rates, there are other costs that you need to keep in mind when you’re evaluating a credit card payment processor.

I’m referring to things like hardware, POS systems, and payment terminals. Some providers charge extra for international transactions, setup fees, or cancellations.

So make sure you review all of this before you decide on service based on the transactional rates alone.

Conclusion

Every business needs a processing service to accept credit card payments, whether you’re selling in-store, online, or both.

What’s the best credit card processing company? It depends. All credit card processors are not created equally. Here’s a recap of the best processing services for specific instances and business types:

- Stripe — Best credit card processor for online payments.

- Helcim — Best credit card processing service for small business.

- Square — Best POS system with integrated payment processing.

- PayPal — Best for low-volume credit card processing.

- Flagship Merchant Services — Credit card processing with flexible terms.

- Payment Depot — Best high-volume credit card processing service.

- CDGcommerce — Best credit card processor for nonprofits and specialty industries.

- Payline — Best credit card processing for high-risk merchants.

No matter what type of business you have, I’m sure you fall into one of the categories above. I made sure to include something for everyone on my list.

Use this guide to find the best credit card processor for your company.

from Quick Sprout https://ift.tt/2QpSXAO

No comments:

Post a Comment